Apr 11, 2025

As retirement approaches, many individuals face the critical decision of how to manage their accumulated savings to ensure a stable and lasting income. One strategy gaining attention is rolling over a 401(k) into an annuity. This approach can offer guaranteed income, protection against market volatility, and a structured plan for Required Minimum Distributions (RMDs).

Understanding the Retirement Landscape

For many retirees, the transition from saving to spending can be just as daunting as the years spent building their retirement nest egg. As life expectancy increases and the cost of living continues to rise, the question of how to safely and efficiently draw down retirement funds becomes one of the most important decisions a person will make in their later years. Fortunately, with the right strategy in place, retirees can enjoy the fruits of their labor while still ensuring their assets last throughout their retirement.

One of the biggest concerns retirees face is running out of money too soon. According to a 2023 Allianz Life study, 61% of Americans fear outliving their retirement savings more than they fear death itself. This fear isn’t unfounded. Market volatility, unexpected healthcare expenses, inflation, and Required Minimum Distributions (RMDs) can all work against a stable retirement. That’s where strategic withdrawal planning and financial tools like annuities can help bring peace of mind.

Rolling over a 401(k) into an annuity is an increasingly popular option for those looking to secure guaranteed lifetime income. Unlike 401(k)s, which are subject to market performance, annuities can offer consistent, predictable payments for life. This predictable income stream acts almost like a personal pension, ensuring that retirees receive monthly deposits regardless of market downturns. Furthermore, fixed indexed annuities have the added benefit of growth potential tied to market performance, without the risk of losing principal. This means your money can grow when the market does well, but it won’t shrink when the market takes a hit.

Another benefit of moving money from a 401(k) into an annuity is simplifying the distribution process. With a 401(k), retirees are responsible for making decisions on how much to withdraw and when. This not only creates stress, but also increases the risk of overspending or triggering unnecessary taxes. An annuity automates the process, creating structure and reducing emotional decision-making. For retirees who value simplicity and a sense of financial routine, annuities can be a welcome solution.

Required Minimum Distributions (RMDs) are also a significant factor in retirement income planning. Starting at age 73, account holders must begin taking minimum withdrawals from their qualified retirement accounts or face substantial penalties. Failing to properly plan for RMDs can not only create an unexpected tax bill but may also result in depleting retirement funds quicker than expected. Certain annuities are RMD-friendly, meaning they can be structured to satisfy RMD requirements automatically while still preserving long-term income.

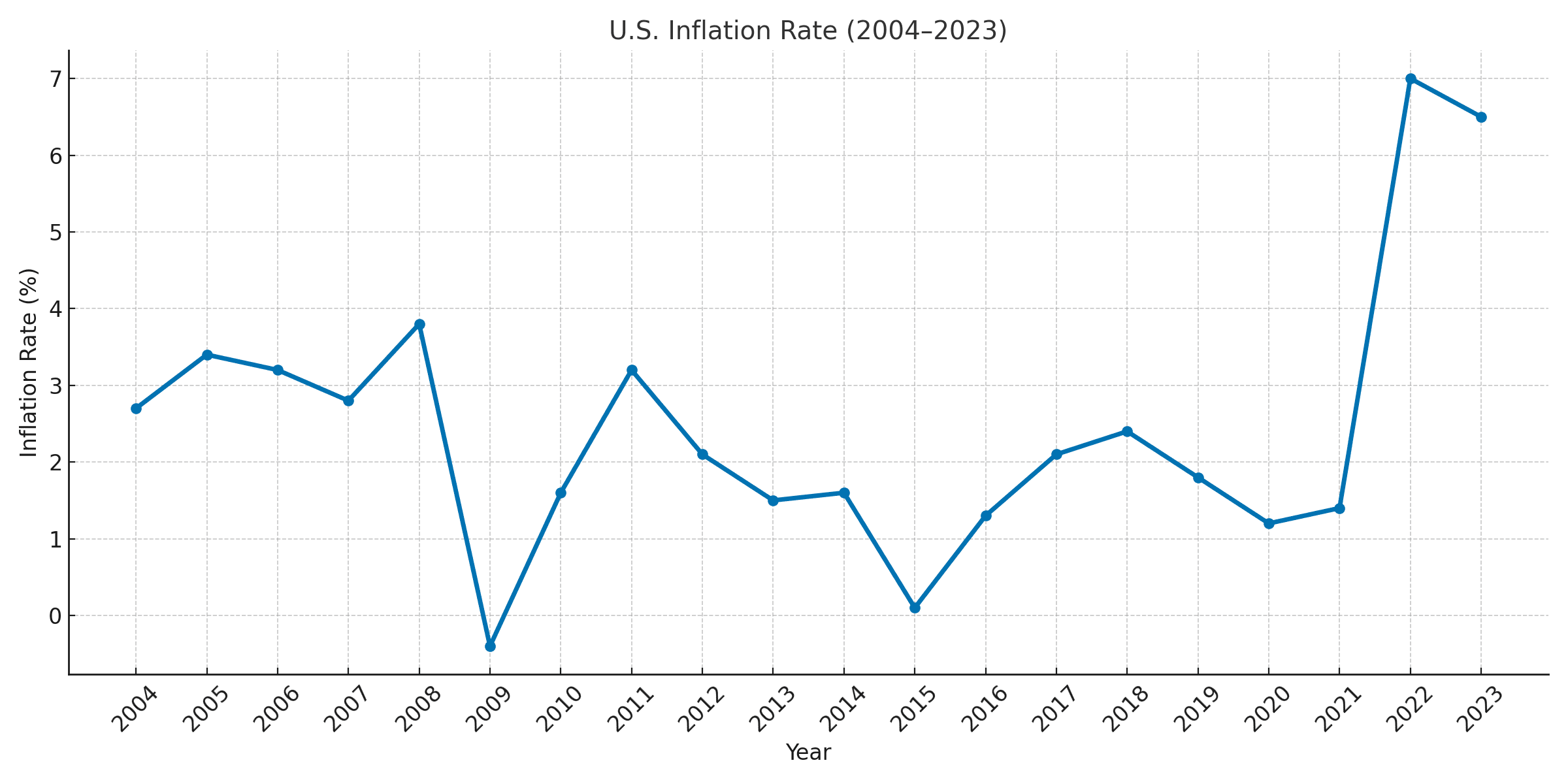

Inflation is another major factor retirees must contend with. Over the past five years, inflation has risen at rates not seen in decades, peaking at 8.0% in 2022 before settling back to more manageable levels. Even modest inflation can erode purchasing power over time, making it critical to have a plan that accounts for rising costs. Some annuities offer inflation-adjusted income, helping retirees maintain their lifestyle without constantly worrying about cutting expenses. Others allow partial market participation, meaning the income can increase based on positive index performance, acting as a hedge against inflation.

Beyond just financial concerns, there’s also the emotional side of retirement planning. Peace of mind is hard to quantify but incredibly valuable. Knowing that you will have money coming in every month, regardless of what happens in the stock market or the economy, allows retirees to truly enjoy their retirement years. Traveling, spending time with grandchildren, or simply relaxing without financial stress becomes more possible when income is guaranteed.

It's also worth noting that annuities are not one-size-fits-all. The decision to roll over a 401(k) into an annuity should be made based on an individual's overall financial picture, goals, and risk tolerance. For example, someone who has significant other sources of guaranteed income (like Social Security or a pension) may want to use a portion of their 401(k) for growth investments, while someone with more modest means may benefit from the security that an annuity provides. Working with a licensed financial professional can help retirees evaluate their options and choose the right blend of income-producing and growth-focused strategies.

Considerations Before Rolling Over

While annuities offer numerous benefits, it's essential to consider potential drawbacks:

Fees and Charges: Some annuities come with fees that can affect overall returns.

Liquidity: Annuities may have surrender periods during which early withdrawals incur penalties.

Complexity: Understanding the terms and conditions of various annuity products can be challenging.

It's crucial to consult with a financial professional to determine if an annuity aligns with your retirement goals and financial situation.

Conclusion

Rolling over a 401(k) into an annuity can be a strategic move for retirees seeking stability, guaranteed income, and protection against market volatility. By understanding the benefits and potential drawbacks, and consulting with financial professionals, retirees can make informed decisions to secure their financial future.

Ready to explore if a 401(k) rollover into an annuity is right for you? Schedule a free consultation with Nemnich Life and Wealth today to discuss your retirement strategy.

The information provided on this website, www.nemnichlifeandwealth.com, is for general educational and informational purposes only and is not intended as legal, tax, investment, or financial advice. All decisions regarding insurance and financial products should be made with the guidance of a qualified professional who understands your personal needs and situation.

Nemnich Life and Wealth, and its representatives, make no warranties regarding the completeness, accuracy, or reliability of any content presented on this site.